The perpetual preferredPerpetual PreferredFixed-income instrument with no maturity that pays a fixed dividend, ranking ahead of common shareholders.View term → shares that fund the two Bitcoin treasuries most active in fixed income —Strategy and Strive— have fallen hard in recent days, and what matters isn't only how much, but where: well below the $100 par value they were designed for.

According to the closing prices SatsIntel tracks, STRC (Stretch), Strategy's third preferred and the first with a monthly payment, closed at $80.84, down from $87.31 the prior session. It's trading 19% below its $100 par. Strive's SATA —a variable-rate preferred, today at 13% annually— closed at $88.56 from a prior $94.50, 11% below par.

Why trading below par matters

This isn't a technical detail. Both preferreds were explicitly structured to trade near $100. That's the key piece of their design: when a preferred trades around par, the issuer can run continuous ATM (at-the-market) programmes —issuing more shares into the market— and raise capital efficiently to buy more Bitcoin. It's the funding engine of the flywheel: issue preferreds at par, buy BTC, repeat.

When those same preferreds slump to $80 or $88, the engine seizes up. Issuing new shares below par is more expensive and more dilutive, and it raises the cost of capital just when the sector needs it most. A perpetual preferred has no maturity: its price depends almost entirely on the relationship between its fixed coupon and market rates, plus the perceived risk of the issuer.

What's behind the drop

Two forces push in the same direction. On one hand, a rising-rate environment makes fixed coupons less attractive: if the market demands more yield, the price of a fixed-coupon instrument falls to adjust the yield. On the other, Bitcoin's recent drawdown pressures the issuers —Strategy and Strive are, at heart, leveraged bets on BTC— and revives doubts about the coverage of high dividends (11.5% monthly on STRC, 13% on SATA) if the flow of capital slows.

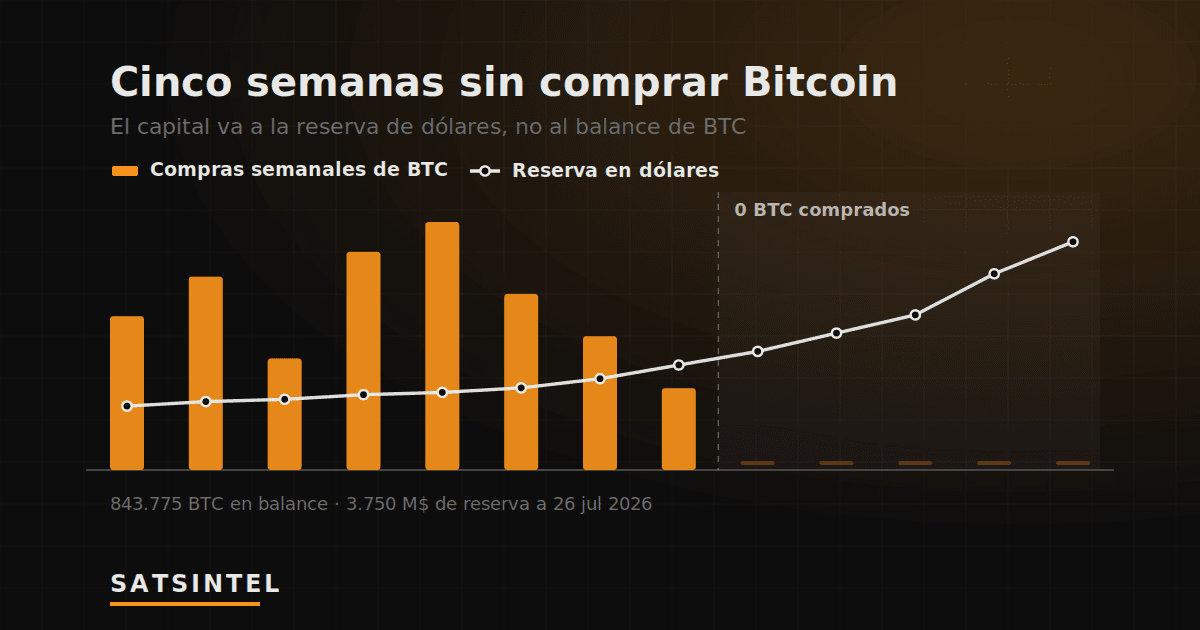

STRC was already in the spotlight in June, when Strategy sold 32 BTC —its first sale since 2022— precisely to cover its dividend payment. That gesture, tiny in volume but huge in symbolism, pointed to the same strain now reflected in the price.

What to watch

The question isn't whether STRC and SATA will return to par, but whether the issuers can keep feeding the flywheel with the preferreds far from par. As long as they trade at a discount, the ATM route loses efficiency and Bitcoin accumulation gets more expensive. You can follow the live price and yield of each instrument in SatsIntel's comparator of Bitcoin-backed preferreds.

Closing data collected by SatsIntel on June 25, 2026. This is educational content, not financial advice.